Background of Issue

There are three types of billing engagements you have with your clients:

- Time Charge Agreements, where you invoice the timesheets to create an invoice.

- Time Charge Agreements, where you invoice a quoted or agreed fee, irrespective of the timesheets on the job.

- Fixed Price Agreements, where you setup a repeating monthly invoice in Xero for the contract value.

What we are focusing on here is the Fixed Price Agreements. For these engagements, we have an agreed fixed fee with our client, to be billed over a 12 month period. We setup a repeating invoice in Xero, and map this revenue to a job within XPM.

There are three possible ways to setup these agreements:

- In Advance

- Contract Period

- Current Period

In Advance when we bill for the annual accounts a year in advance. It’s the best method for cashflow, but the most difficult to onboard new clients due to the heavy up front fees involved.

Contract Period is where we have contract renewal dates which do not have any alignment with the clients financial year. It is much easier for onboarding new clients, but can require a bit more administration.

Current Period is where we bill for the work we do in the 12 months. It is the worst option for cashflow, but the easiest way to on board new clients.

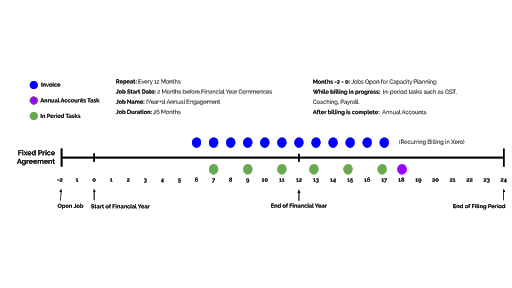

Option One - In Advance

When using the ‘In Advance’ method, we bill for the annual accounts in advance, and the in-period tasks such as GST and payroll during the year which the billing is incurred. So the engagement can last up to 24 months, spanning across two financial years. The first 12 months is for the in-period tasks, while the last 12 months is for the annual accounts.

It’s important to note that we are accumulating negative WIP using this method as we are billing in advance. This negative WIP is a liability to us as we have not yet done the work that we have collected the fees for. At the end of the financial year, we would have collected all the fees for next years work. This is great for cashflow, but it is important to recognise the corresponding liability.

Here is a diagram that shows how this works:

Note that this diagram shows the job being created two months before the financial year starts. This allows the practice to schedule all the tasks on the job in the two months leading up to the start of the financial year. The alternative is to have the job open on the first day of the start of the financial year. If this option is chosen, scheduling will have to be done once the financial year has started.

It is good practice to update the due date of the job when the client brings their info in. When the job is created, it will have a due to to be the end of the following financial year - which is when the filing is due. It is a good idea to update this due date when the client brings in their records to be 4 - 6 weeks out, which is the amount of time we would expect the turn the job around.

Once the annual accounts and tax returns have been completed and filed, the job can have the WIP washup applied by hitting ‘Remove from Invoice List’, then the job can be closed.

So what happens when a client comes on board half way through a financial year?

Let’s say a client signs up with us 5 months into the financial year 2020 financial year. Under this method we would complete the 2019 annual accounts on a quoted or a time and cost basis. For the 2020 annual accounts we would setup a recurring payment for the rest of the 2020 financial year and the work will be completed in the 2021 year. But we need to recognise there has been 5 missed installments. We have two options here, we can either bill these up front when the client signs up, or we can increase their next 7 installments to account for the 5 missed ones. Once we hit the 2021 year, we can reduce these installments to 1/12 of the agreed fee for the annual engagement.

Option Two - Contract Period

When using the ‘Contract Period’ method, we bill the annual accounts and tax returns in advance, and the in-period tasks such as GST and payroll during the year which the billing is incurred. How this differs from the ‘In Advance’ method, is we do not backdate the billing to the start of the financial year. Instead, we have the renewal date on the same month each year.

Let’s say we have a client sign up in the 5th month of the financial year. Under the ‘In Advance’ method, we would backdate 5 months of billing to align this with the client's financial year. Whereas under the ‘Contract Period’ method, we identify the renewal date, and will not start the annual accounts until all 12 installments have come in. This also helps with scheduling the work, because we know we work on this clients accounts in month 5 of the next financial year.

This method also accumulates negative WIP as per the ‘In Advance’ method.

Here is a diagram that shows how this works:

Note that this diagram shows the job being created two months before the financial year starts. This allows the practice to schedule all the tasks on the job in the two months leading up to the start of the financial year. The alternative is to have the job open on the first day of the start of the financial year. If this option is chosen, scheduling will have to be done once the financial year has started.

The key to this method is to move the billing from the previous engagement to this new engagement on the renewal date. In this diagram the billing starts for the new engagement on the 6th month. So the billing on the 5th month would would be the 12th installment on the last engagement. At that stage we want to update our billing to send the invoice to this job. To understand how to do this refer to our guide on ‘Invoicing Fixed Price Agreements from Xero’.

You will need to keep track of your renewal dates so you can do the changeover. This can be done using a custom field in XPM, or a standalone spreadsheet. You will have a list of clients you need to change the billing over for each month.

Like the ‘In Advance’ method, it is good practice to update the due date of the job when the client brings their info in. When the job is created, it will have a due to to be the end of the following financial year - which is when the filing is due. It is a good idea to update this due date when the client brings in their records to be 4 - 6 weeks out, which is the amount of time we would expect the turn the job around.

Once the annual accounts and tax returns have been completed and filed, the job can have the WIP washup applied by hitting ‘Remove from Invoice List’, then the job can be closed.

So what happens when a client comes on board half way through a financial year?

Let’s say a client signs up with us 5 months into the financial year 2020 financial year. Under this method we would complete the 2019 annual accounts on a quoted or a time and cost basis. This is the same as the ‘In Advanced method. For the 2020 annual accounts we would setup a recurring payment for the rest of the 2020 financial year and the work will be completed in the 2021 year.

Unlike the ‘In Advance’ method, we would not backdate the missing 5 installments. We just note down the renewal date and ensure we don’t start their work until we have collected the 12 installments. If the client would like to get their accounts done earlier, we can invoice them for the missing installments which would update their renewal date by the number of periods we invoice for.

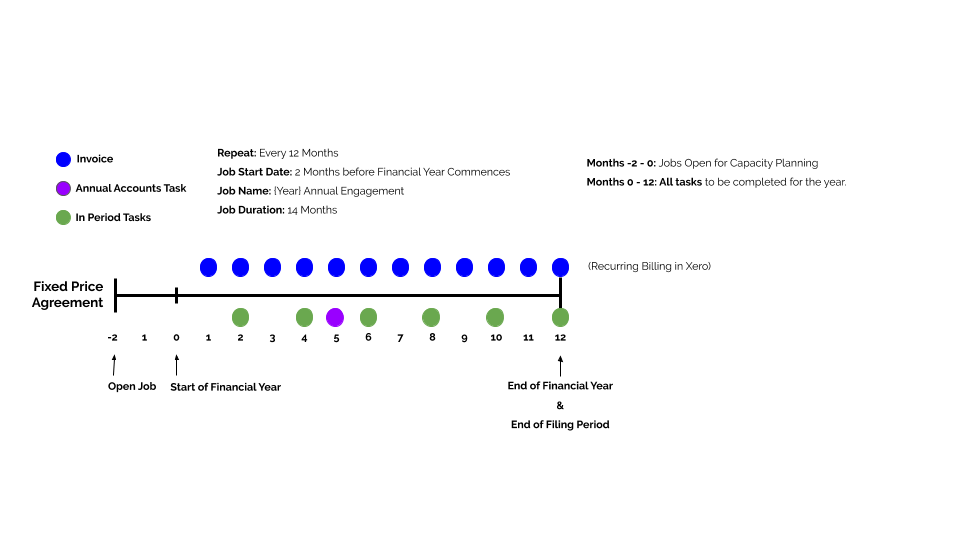

Option Three - Current Period

When using the ‘Current Period’ method, we bill for the annual accounts in the same year we are completing them. For example, we would be billing for the 2020 annual jobs during the 2021 year. Which differs from the other two methods. The other two methods we are billing for the 2020 in the 2020 year so we collect the funds up front, then do the work. Whereas under the ‘Current Period’ method we are completing the work while the client pays for it over a 12 months period.

The downside of this method is we might finish the annual accounts in month 2, but the client is paying the work off over the following 10 months. The counterargument to this, is some clients will have their work completed in month 1 and some in month 12, so it all works out at year end, as long as the monthly fees are covering monthly salaries.

This method accumulates negative WIP against the jobs that we have not worked on yet, and positive WIP for jobs that have been completed. At year end we would expect to have no negative WIP, therefore no large liability.

Here is a diagram that shows how this works:

Note that this diagram shows the job being created two months before the financial year starts. This allows the practice to schedule all the tasks on the job in the two months leading up to the start of the financial year. The alternative is to have the job open on the first day of the start of the financial year. If this option is chosen, scheduling will have to be done once the financial year has started.

The annual accounts task shown in the diagram is for the previous financial year. In the other two methods, we showed the annual accounts task being competed in the next financial year because it was billed in advance, whereas under the ‘Current Period’ method, we are billing for the work we are completing in this financial year, and spreading the payment over the 12 months.

So what happens when a client comes on board half way through a financial year?

It is easier to onboard clients using this method because we are not billing anything in advance. Instead we have two options. We can do this first year on a time and cost basis, then move a month service plan next financial year, or we can start the monthly subscription payments from the signup date, then invoice the missing payments up front.

So let’s say we have a client sign up in month 5 of the financial year. We could start them on a monthly subscription from month 6 onwards, and send an invoice for months 1 - 5. Alternative we could charge a ⅕ loading on each of the remaining 7 invoices so we have collected all 12 installments by the end of the 12 months.

In Summary

Each method has it upsides and drawbacks.

The ‘In Advance’ method is the best for cashflow, but it can be difficult to onboard new clients due to the higher upfront fees. It also carries a bigger risk due to the negative WIP liability at year end.

The ‘Contract Period’ is a good middle ground. It is easier to onboard new clients, but doesn’t mean you are bankrolling your customers for up to 12 months. You still have a negative WIP liability, but it is spread throughout the financial year. It is also great for cashflow because you are being paid in advance.

The ‘Current Period’ method is the easiest way to onboard clients, but it can leave you in a big cash hole. If you bring on a lot new clients you are likely to be trading from an overdraft because you have to pay wages now, but you are not getting paid for up to 12 months. It is the safest in terms of negative WIP liability, but you will be paying interest to the bank to keep on top of wages.

Our preferred method is the Contract Period. It allows you to get paid up front for you work, but it doesn’t make your onboarding difficult. It is a perfect balance of the two other methods.

Comments

0 comments

Please sign in to leave a comment.