This article is an extract from the book 'Everything you need to know about Xero Practice Manager'

Get a copy for your desk at www.linkedpractice.com

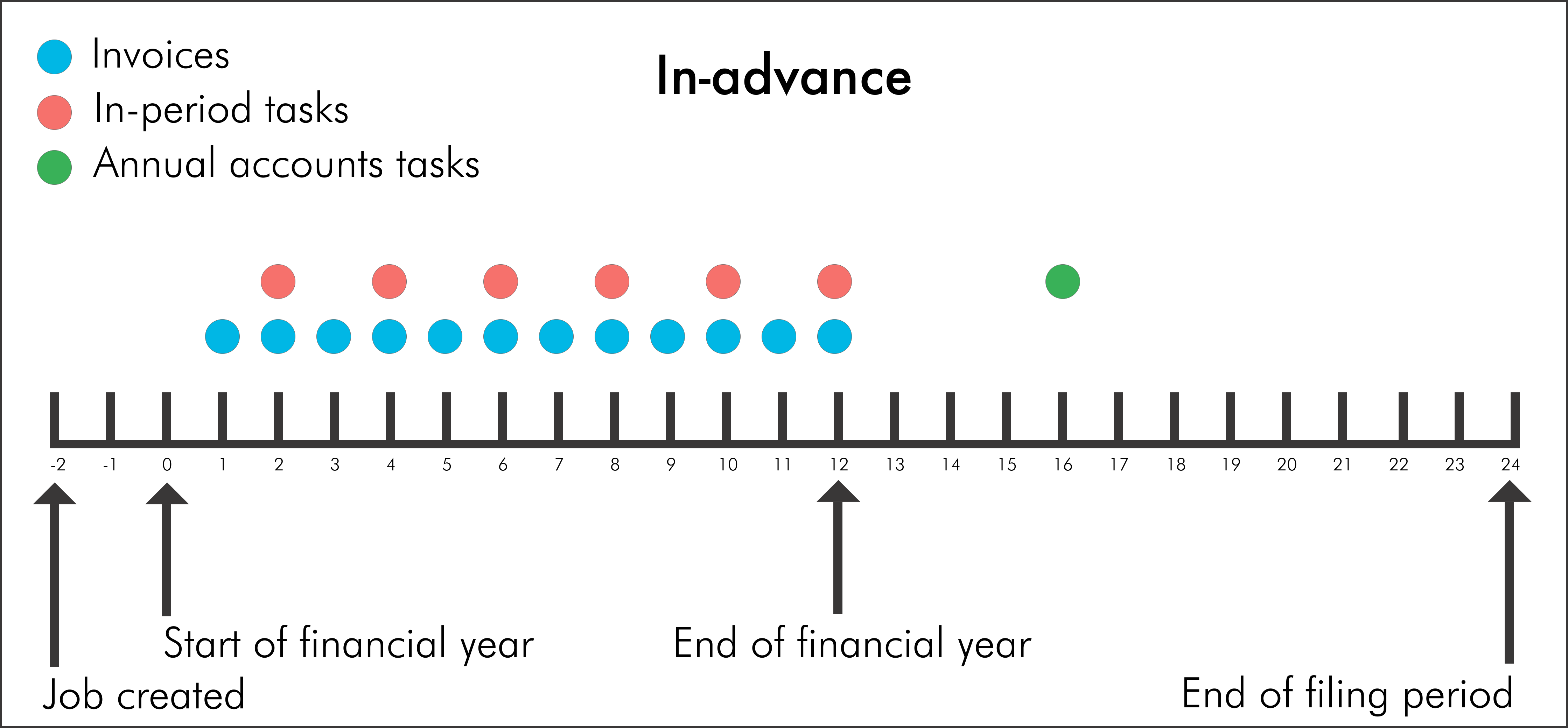

In-advance is when we bill for the annual accounts work a year in advance. So we are collecting the full 12-month installments before we start working on the annual accounts. This is the best method for cash flow, but the most difficult to onboard new clients due to the higher up-front fees involved

When using this method, we bill for the annual accounts in advance. So if we are in the 2020 financial year, we will bill for this year then start the work in the 2021 financial year. When we do this, we would have collected all the funds up front for the work to be done. The client is therefore paying their accounting fee in advance.

It is also worth noting here that any in-period tasks such as GST or payroll are billed during the year in which they are incurred. So billing in the 2020 financial year covers the GST and payroll for the 2020 financial year, and the 2020 financial statements. It just happens that the financial statement work is done in the 2021 financial year.

Because we are billing for the in-period tasks throughout the year, and prepaying the annual accounts, these engagements can last up to 24 months, spanning across two financial years. The first 12 months is for the in-period tasks, while the other 12 months is for the annual accounts.

It is important to note that we are accumulating negative work in progress (WIP) using this method as we are billing in advance. This negative WIP is a liability to us as we have not yet done the work that we have collected the fees for. At the end of the financial year, we would have collected all the fees for next year's work. This is great for cash flow, but it is important to recognise the resulting liability.

Let’s look at an example:

Say we have a client for whom we complete both GST and annual accounts work, and we are charging the client $500 per month (being $6,000 for the full year's engagement). At the start of the 2020 financial year we will have billed nothing, and done no work, so our WIP is $0. After the first month we will have billed $500 and still have done no work, so our WIP is now negative $500, which is shown as ($500).

At the end of the second month we will have completed the first GST return for the year, which incurred $300 of billable time. We will have also billed another $500. So we have billed $1,000 so far, and put $300 of time on the job, so our WIP is negative $700.

At the end of the financial year, we will have billed $6,000 and put $1,200 of billable time on the job for the GST work. This means we have a negative $4,800 of WIP on the job, which is our budget to complete the annual accounts work in the next financial year.

Following is a diagram that illustrates how this works:

Note that this diagram shows the job being created two months before the financial year starts. This allows the practice to schedule all the tasks on the job in the two months leading up to the start of the financial year. The alternative is to have the job open on the first day of the start of the financial year. If this option is chosen, scheduling will have to be done once the financial year has started. This will be covered in more detail in Chapter 7: Setting up Engagements. For now, just focus on the invoices, and when the tasks are completed.

Enjoy this article? Buy the book.

Need help setting up, fixing up, or getting up to speed on Xero Practice Manager?

We can help at www.linkedpractice.com

Comments

0 comments

Please sign in to leave a comment.